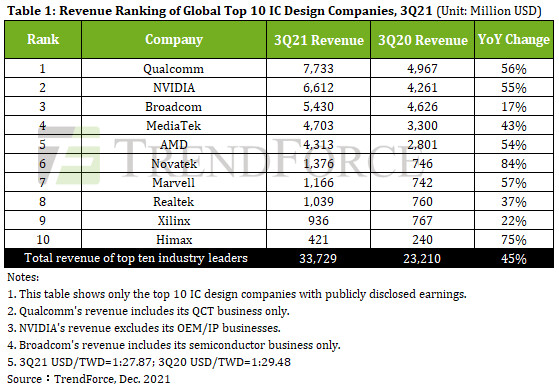

3Q21 Revenue of Global Top 10 IC Design (Fabless) Companies Reach US$33.7 billion, Four Taiwanese Companies Make List, Says TrendForce

Qualcomm has been buoyed by continuing robust demand for 5G mobile phones form major mobile phone manufacturers with further revenue growth from its processor and radio frequency front end (RFFE) departments. Qualcomm’s IoT department benefited from strong demand in the consumer electronics, edge networking, and industrial sectors, posting revenue growth of 66% YoY, highest among Qualcomm departments. In turn, this drove Qualcomm’s total 3Q21 revenue to US$7.7 billion, 56% growth YoY, and ranking first in the world.

Second ranked NVidia, is still benefiting from gaming graphics card and data center revenue as the annual revenue growth for these two primary product departments reached 53% and 48%, respectively. In addition, professional design visualization solutions only accounted for 8% of total revenue. However, due to enduringly strong demand for mining and customers actively deploying the RTX series of high-performance graphics cards, NVidia’s product department revenue grew 148% YoY with overall revenue increasing by 55% to US$6.6 billion.

Third ranked Broadcom’s main revenue stream came from their network chip, broadband communication chip and storage and bridge chip businesses. Driven by post-COVID hybrid working models, companies are accelerating migration to the cloud, increasing demand for Broadcom chips, and driving revenue growth to US$5.4 billion or 17% YoY. AMD’s Ryzen, Radeon, and EPYC series of products in the fields of games, data centers, and servers performed well, driving total revenue to US$4.3 billion, 54% growth YoY, and fifth place overall.

In terms of Taiwanese companies, MediaTek continues to expand its global 5G rollout and, benefiting from optimization of product portfolio composition, product line specification enhancement, increase in sales volume, increases in pricing, and other factors, revenue of MediaTek’s mobile phone product line increased 72% YoY. Annual revenue of other product lines also posted double digit growth with total revenue in the 3Q21 reaching US$4.7 billion or 43% YoY, a fourth place ranking. Novatek continues to focus on its two primary product lines of system-on-chip and panel driver chips. The proportion of its OLED panel driver chip shipments has increased, product ASP has risen, and shipments have been smooth with 3Q21 revenue reaching US$1.4 billion or 84% YoY. In addition, Realtek’s revenue surpassed Xilinx to take the eighth position due to higher priced Netcom chips in 3Q21. Himax also saw significant growth in its three main product lines of TVs, monitors, and notebooks due to large-size driver chips. Revenue from large-size driver chips increased 111% YoY, driving total revenue to exceed the US$400 million mark, a 75% increase, and enough to squeeze onto this year’s ranking.

Overall, 3Q21 revenue for major IC design (fabless) companies has generally reached historic levels. Rankings for the top 7 companies remained the same as in 2Q21 with change coming in ranks 8 to 10. Looking forward to 4Q21, TrendForce believes Taiwanese IC design (fabless) companies will generally lean conservative. In addition to the electronics industry moving into the traditional off-season, a slowing of demand for consumer applications and customer-end materials supply issues reducing procurement will make continued revenue growth a challenge. In addition to consumer electronic products, global industry leaders are focused on the positive development of server and data center products to maintain an expected revenue growth trend.