Server Shipments Forecast to Increase 4~5% YoY in 2022 Driven by North American Data Center Demand, Says TrendForce

TrendForce states, based on the current situation as materials issues ease quarter by quarter, the annual growth rate of server shipments in 2022 will reach 4~5%. There are three primary factors driving market momentum. First, the introduction of the Intel Sapphire Rapids and AMD Genoa platforms into the market may once again stimulate the replacement of enterprise client servers and infrastructure construction in data centers. Second, the market generally believes that transformational needs generated by the pandemic in 2022, such as shifts in working paradigms and the new normal, will continue to drive the cloud market. Furthermore, international tensions have led to geopolitical uncertainty, which in turn has encouraged countries to tighten their control over data sovereignty and prompting the emergence of small-scale data centers in specific geographic locations.

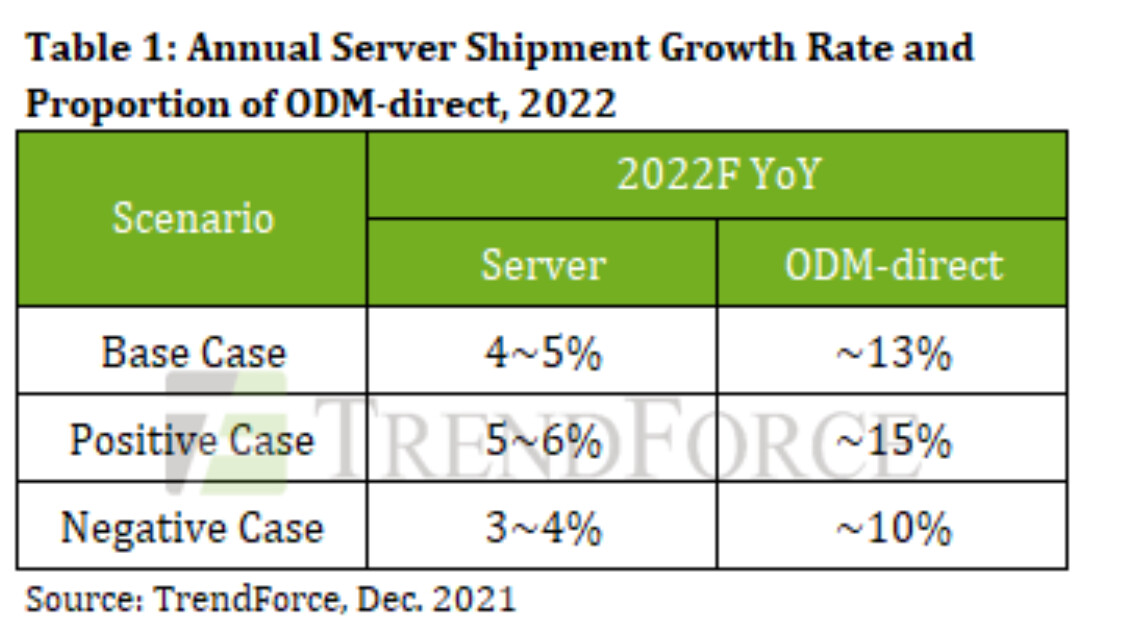

Actual shipment volume of completed servers in 2022 depends on improvement of supply chain issues

Based on the two aforementioned assumptions, if the pandemic is effectively controlled next year, and international logistics, satisfaction of materials demand, and other factors either return to normal or fare better than expected, server companies will be able to increase their shipping capabilities and the annual growth rate of shipments in the overall server market will be able to reach 5-6% while the annual growth rate of ODM-Direct will approach 15%, up from the original forecast 13%. However, if the pandemic intensifies next year, the overall global economy will continue under that dark cloud which will greatly affect the willingness of companies to invest. In that case, the estimated annual growth rate of server shipments will fall to only 3-4%. In addition, the growth momentum of North American data centers will also be affected leading to an annual growth rate of ODM-Direct of only 10%, approximately.

As a whole and continuing under the influence of the two-year pandemic, the business trend of flexible deployment is irreversible. Regardless of overall economic changes, TrendForce expects double-digit growth in the demand for ODM-direct servers next year while overall server demand will also maintain a positive growth trajectory. However, continued attention should be focused on issues related to server order fulfillment in the broader market, including the fulfillment rate of key PMIC and LAN chip materials. At the same time, another major market variable will be whether Intel and AMD can introduce their two new platforms as scheduled next year and inject additional momentum into equipment replacement.