World’s Top Ten IC Design Company Revenue Reached US$39.43 billion in 1Q22, Marvell Growth Rate Tops List, Says TrendForce

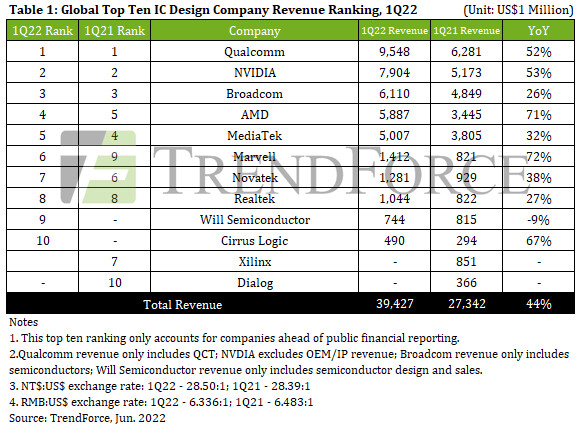

Benefiting from growth performance in handsets and RF front-end divisions in addition to its IoT and automotive divisions in 1Q22, Qualcomm’s quarterly revenue reached US$9.55 billion, or 52% growth YoY, ranking number one in the world. The expanded application of GPUs in data centers boosted this portion of NVIDIA’s revenue to 45.4%, surpassing the 45% accounted for by its gaming business, combining for a total revenue of US$7.9 billion, or 53% growth YoY. Broadcom’s revenue from semiconductor solutions is substantial, including network chips, broadband communication chips, and storage and bridging chips. Its business has maintained stable sales performance, with revenue reaching US$6.11 billion, or 26% growth YoY. After the addition of Xilinx, AMD’s revenue reached US$5.89 billion, or 71% growth YoY. However, even excluding Xilinx, due to strong sales in its enterprise, embedded and semi-customized divisions, AMD’s own business revenue still hit an all-time high of US$5.33 billion.

In terms of Taiwan-based companies, MediaTek’s Dimensity series processors have been shipped at volume and their product mix has been optimized successfully, pushing revenue to US$5.01 billion, or 32% growth YoY. Novatek’s business is based on display driver IC and SoC. Even though revenue was bogged down by sluggish panel demand, the company’s two major product lines still achieved annual growth of 31% and 43%, respectively, with a total revenue of US$1.28 billion, or 38% growth YoY. Realtek made up for the relatively weak demand for consumer products through its dynamic commercial product portfolio which includes Ethernet chips, switch controllers, and WiFi chips, totaling revenue of US$1.04 billion, or 27% growth YoY.

Marvell jumped to sixth place this quarter, as its acquisition of cloud and edge data center networking solutions provider Innovium in October 2021 contributed 125% annual growth to its 1Q22 data center revenue, bringing total revenue to US$1.41 billion, or 72% growth YoY, highest among the top ten. Will Semiconductor, a newcomer to the list, is headquartered in Shanghai, China. Its semiconductor design and sales revenue accounts for approximately 85.1% of total revenue. The company’s main products are CMOS image sensors, display driver ICs, and analog ICs. Although it is affected by the mobile phone market and revenue fell 9% YoY, it still reached US$744 million, ranking ninth. As for Cirrus Logic, headquartered in Texas, USA, the company has two major product lines: audio and mixed-signal. After the acquisition of Lion Semiconductor in July 2021, Cirrus accelerated the improvement of its mixed-signal business, driving 1Q22 revenue to US$490 million, or 67% growth YoY, ranking tenth.

TrendForce indicates that 1Q22 rankings have changed due to strategic mergers and acquisitions by a number of players. However, in addition to direct revenue growth brought about by acquisitions, it is still necessary for M&A synergy to be improved in the future. Looking to 2Q22, as the traditional industry off-season dawns, coupled with the impact of rising inflation, the Russian-Ukrainian war, China’s lockdowns, and weak consumer confidence, IC design companies with a high proportion of consumer electronics revenue will see unfavorable results. This is evident from the M&A strategy employed by various industry players that has gradually diverted their product applications to markets such as high-performance computing, servers, data centers, and automotive electronics in an effort to diversify operational risks. In addition, the performance of companies including Synaptics, LX Semicon, and Himax is also worth observing and rankings may change in 2Q22.