Jon Peddie-Forschung: Auslieferungen von Grafikkarten im dritten Quartal steigen um 12% Jahr für Jahr

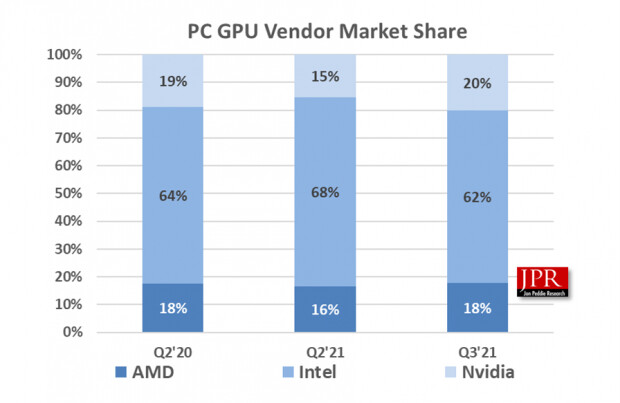

AMD’s overall market share percentage from last quarter increased 1.4%, Intel’s market share decreased by -6.2%, and Nvidia’s market share increased 4.86%, as indicated in the following chart.

Overall GPU unit shipments decreased by -18.2% aus dem letzten Quartal, AMD shipments decreased by -11.4%, Intel’s shipments decreased by -25.6%, and Nvidia’s shipments increased 8.0%.

Quick highlights

- The GPU’s overall attach rate (which includes integrated and discrete GPUs, Desktop, Notizbuch, und Arbeitsplätze) to PCs for the quarter was 125%, oben 7.6% aus dem letzten Quartal.

- The overall PC CPU market decreased by -23.1% quarter-to-quarter and increased 9.2% year-to-year.

- Desktop graphics add-in boards (AIBs that use discrete GPUs) increased by 10.9% from the last quarter.

- This quarter saw a -6.9% change in tablet shipments from last quarter.

The third quarter used to be the strongest relative to Q2, but recessions and pandemics have scrambled seasonality. Even so, this quarter was the lowest ever, from the previous quarter. This quarter was down -18.2% from last quarter which way is below the 10-year average of -5.2%.

GPUs are traditionally a leading indicator of the market because a GPU goes into a system before the suppliers ship the PC. Most of the semiconductor vendors are guiding up for the next quarter, ein Durchschnitt von 2.7%. Last quarter they guided -1.5% which was too high.

Average selling prices remain high as supply is still constrained.

The low-end of the notebook market is saturated with Chromebooks resulting in an ironic inventory buildup during a short-supply situation.

The discrete notebook market has benefited and suffered due to COVID. Notebook sales surged as people stayed home to work. Then Chromebooks took off and undermined the low-end of notebooks GPUs. It will take until Q1 ’22 to get back to normal, if then.

Jon Peddie, President of JPR, notiert, “Covid continues to unbalance the fragile supply chain that relied too heavily upon a just-in-time strategy. We don’t expect to see a stabilized supply chain until the end of 2022. Inzwischen, there will be some surprises.”

Most of the semiconductor vendors are guiding up for the next quarter by an average of 3%. Some of that guidance is based on normal seasonality, but there is still a Coronavirus impact factor and a hangover in the supply chain.

JPR also publishes a series of reports on the graphics Add-in-Board Market and PC Gaming Hardware Market, which covers the total market, including system and accessories, and looks at 31 Länder.