NAND-Flash-Markt im dritten Quartal 22 überversorgt, Preisnotierungen sollen um 0 bis 5 % sinken, Sagt TrendForce

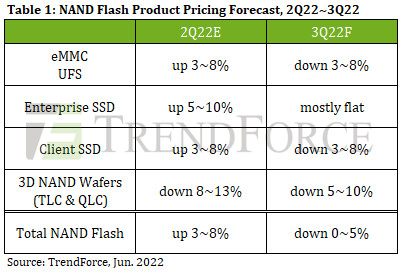

In terms of Client SSD, although a backstop for business notebook orders remains, demand for consumer notebook and Chromebook orders lags behind 2021, especially as PC brands stock more conservatively. Their intention to actively reduce inventory is obvious and the volume of orders in peak season may fall behind last year. Jedoch, as SSD production capacity gradually returns to normal, supply of client SSDs continues to increase. Außerdem, shipments of Kioxia and WDC products been delivered in succession. In order to avoid a sharp increase in inventory, the supply side is willing to let prices spike. Client SSD pricing is expected to reverse direction and move downwards approximately 3-8% in 3Q22.

In terms of Enterprise SSD, purchase orders from hyperscale data centers remain strong and, compared with other products, Kunden’ enterprise SSD inventory levels are still reasonable, inducing sustained growth in SSD purchases. Global enterprise SSD purchase capacity can be expected to grow by 10% QoQ in 3Q22. Due to rapidly weakening demand for other end products, enterprise SSDs are currently the preferred sales category for all suppliers. Increased supply will inevitably intensify price competition. As a result, enterprise SSD prices are not likely to rise in 3Q22 and remain roughly in line with 2Q22.

In terms of eMMC, demand for Chromebooks has continued to decline since 2Q22. Although the demand for Netcom products in 3Q22 is relatively optimistic, it is still no match for the downward trend of eMMC pricing. The impact of the prior raw material contamination incident on the broader market has gradually faded. In a climate of poor consumer product demand, it is difficult for suppliers to support 2D eMMC product pricing to maintain profitability. Due to the current state of oversupply, eMMC prices are predicted to drop by 3-8% in 3Q22.

In terms of UFS, the trends of sluggish smartphone shipments and cooling of the consumer market remain unchanged, suppressing the growth trend of bit demand. The impact of the Kioxia/WDC raw material contamination incident at the beginning of the year on the total output of 3D NAND has gradually faded. With the recovery of production capacity at the aforementioned companies, the supply of UFS products has been stable. Prices are starting to come under pressure amid a weak demand outlook and rising supply. Judging from the current demand situation, even if suppliers dole out large price reductions, the effect on demand stimulation remains very limited. Deswegen, the price of UFS is predicted to drop by 3~8% in 3Q22 and the number of bits sold will remain at a low level.

In terms of NAND Flash wafers, expecting a drop in pricing, the number of wafer purchases in 3Q22 has an opportunity to rebound in comparison to 2Q22 as the curtain falls on peak season and the pandemic in China. Gleichzeitig, the impact of flagging upstream supply has gradually faded and the supply side has continued to expand wafer supply. Module manufacturers have begun to adopt an active price reduction strategy to reduce their inventories. In order to narrow the gap between the wafer contract and spot price, companies had begun to simultaneously reduce wafers contract prices in May, while a contraction in contract pricing in June may extend to nearly 10%. Deswegen, as wafer pricing had already fallen in May, 3Q22 decline can be mitigated to 5~10%.