SSD-Lieferungen über globale Vertriebskanäle erreicht 127 Millionen Einheiten ein 2021, Hoch 11% YoY

Dieses globale SSD-Ranking basiert auf dem Versandvolumen von Modulhäusern’ eigene Eigenmarken im Vertriebskanalmarkt als Berechnungsmaßstab und NAND-Flash-Hersteller werden nicht berücksichtigt. NAND Flash manufacturer supply accounts for approximately 42% of the overall distribution channel market while module factory shipments account for approximately 58%. When SSD-related components were hard to come by, NAND manufacturers’ supply chain management occupied a superior position compared to module houses, so NAND manufacturers’ market share in the overall distribution channel market increased compared with 2020.

Looking at changes in the global SSD market in 2021, zuerst, SSDs were in short supply due to a shortage of SSD related components in early 2021 and large module houses adopted a limited supply strategy in response as product prices rose. This increase in overall profit also prompted more module houses to follow suit. Some large module houses obtained support from SSD controller IC manufacturers due to their supply chain advantages, increasing their market share. Zweite, due to an inability to obtain a supply of upstream wafer production capacity in recent years, newly introduced controller ICs from mainland China have become a bottleneck in the supply of SSD controllers for certain Chinese manufacturers. Dritte, the pandemic festers and gaming-related demand remains strong, so the ranking of brands focused on gaming laptop-related products has also moved up.

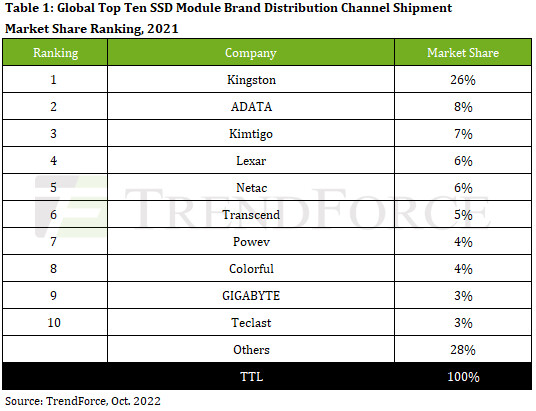

The present ranking of SSD module manufacturers maintains a trend of the rich getting richer with the top three in terms of shipments remaining Kingston, ADATA, and Kimtigo. Of the top three, only Kingston’s market share moved lower. Due to their huge production demand, shipment volume was affected when wafer supply was too limited to meet order lead time. The biggest change on this list is Transcend’s ranking rising sharply from tenth place in 2020 to sixth place, as well as newcomers Powev and GIGABYTE.

Transcend’s long-term brand advantage comes from obtaining support from SSD controller IC manufacturers and the company’s shipments have grown significantly as a result. In particular, its SSD products are specially designed to meet the needs of Apple’s notebook upgrades. As Apple’s laptop market share grows, demand for relevant Transcend products increased and its SSD shipment market share rose to 5% in 2021. Benefiting from its long-term operation in the high-end gaming market and diversified product solutions, Powev entered the top ten as demand for high-end performance and game-related products retains strong growth momentum. Gigabyte also benefited from the company’s efforts to expand the supply of game-related components with its motherboard products driving SSD shipments.

Penetration rate of PCIe specifications continues to rise, global market disposition heralds future growth momentum of various brands

The pandemic continuously disrupted the supply of SSDs in 2021. In addition to the supply of SSD controller ICs, a diversified distribution of production centers was also a key factor in enhancing the momentum of shipments. In die Zukunft schauen, the growth momentum of module factories focused on selling SSD interfaces will gradually shift from SATA to PCIe. Jedoch, Kompatibilitätsprobleme sind aufgrund der um ein Vielfaches höheren Übertragungsgeschwindigkeiten der PCIe-Schnittstelle auch komplizierter als bei SATA-SSDs. Die Bereitstellung umfassender Dienstleistungen zur Unterstützung bei SSD-Produkt-Upgrades kann die Markenbekanntheit steigern und die Auslieferungen weiter steigern. TrendForce glaubt, zusätzlich zu den Kosten, Die Fähigkeit, umfassende globale Produktions- und Vertriebsdienstleistungen anzubieten, wird ein wichtiger Faktor sein, um die PCIe-SSD-Lieferungen in Zukunft weiter zu steigern.

Die Technologie der Speicherprodukte chinesischer Unternehmen verbessert sich weiter, Das Ziel, die SSD-Produktion in China zu lokalisieren, steht vor der Tür

TrendForce hat das auch in der SSD-Lieferkette beobachtet, der Anteil der Lokalisierung in China nimmt zu. Insbesondere in der Controller-IC-Technologie, Eine Reihe von Herstellern hat nach und nach mit der Forschung und Entwicklung von PCIe-Controller-ICs begonnen, und einige Modulhersteller haben sogar mit chinesischen Servern zusammengearbeitet, um SSDs für Unternehmen zu entwickeln. Nachdem Intel begann, sich schrittweise aus dem Angebot an Optane-SSDs zurückzuziehen, ein bestehender chinesischer Hersteller, DapuStor, hat Kioxia XL Flash bereits übernommen, um eine alternative Lösung mit ähnlicher Leistung auf den Markt zu bringen, Ich hoffe, Marktaufträge in diesem Speicher der Speicherklasse zu erfassen (SCM) nach dem Rückzug von Intel. Die obige Entwicklung zeigt deutlich, dass die Rolle chinesischer Hersteller in der SSD-Lieferkette immer stärker wird und dass es in Zukunft Möglichkeiten geben wird, durch Upstream- und Downstream-Integration weiterhin Marktanteile zu gewinnen.