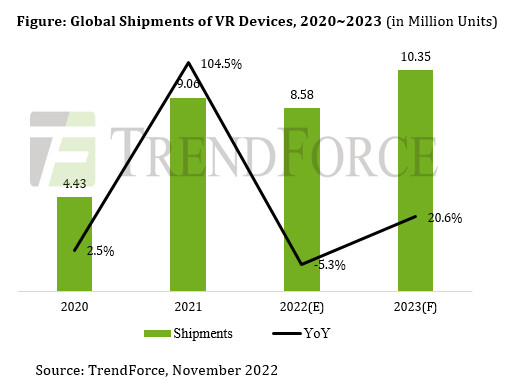

Global Shipments of VR Devices Should Reach 10.35 Million Units in 2023, Says TrendForce

[ad_1]

Meta has been the most aggressive in committing resources into the VR/AR market. However, the effect of its attempt to offer hardware at a low price has been quite disproportionate to its massive investments in related technologies. Due to mounting cost pressure, Meta has adjusted its pricing strategy for Quest devices. The Meta Quest 2, in particular, is now priced at US$1,499, which is more than three times its previous price. On account of this price hike and its relatively short battery life, the Quest Pro will unlikely follow the footsteps of the Quest 2 with respect to maintaining a strong shipment growth momentum. TrendForce estimates that that shipments of the Quest Pro will reach just to the level of 250,000 units for 2022. Meta will have to wait until next year, when the Quest 3 hit the market, to again see a notable positive growth in its shipments of VR devices. TrendForce currently forecasts that Meta’s shipments for 2023 will total around 7.25 million units.

As for Sony, raising the sales of its upcoming PS VR2 to a significant scale will be difficult as the device is targeting the very niche market for gaming products. Nevertheless, PS VR2 will be able to provide a much better VR gaming experience. This has to do with the fact that it is not downward compatible in terms of hardware and software. Moreover, its games will be pure VR games designed to take advantage of the device’s new or more advanced functions such as eye tracking and haptic feedback. Providing an exceptional user experience is going to be Sony’s key to maintaining its market share for VR products. TrendForce forecasts that shipments of the PS VR2 will reach around 1.6 million units for 2023. This particular product will be a major growth contributor in the VR market next year.

Even though shipments of VR devices will rise again next year, the extent of this growth will still be limited due to directions in production development. Currently, the specifications of VR devices are moving towards smaller form factor (i.e., lighter and thinner devices), better performance (such as better image quality), and more sensing functions. These three trends not only have led to a simultaneous rise in both hardware cost and retail price but also discourage other electronics brands from entering the VR market. It is worth noting that even though Meta is still the top brand for VR devices, but its advantages associated with being a market leader are going to diminish due to the increasing cost pressure and the inability to find use scenarios for its products. TrendForce believes that Meta’s competitors can use this opportune moment to capture more market share for VR devices by focusing on entry-level products that can offer a better C/P ratio.

[ad_2]