Tasa de crecimiento interanual proyectada de los envíos de servidores globales para 2023 ha sido rebajado a 1.87% Debido a la reducción de la demanda de los proveedores de servicios en la nube de América del Norte

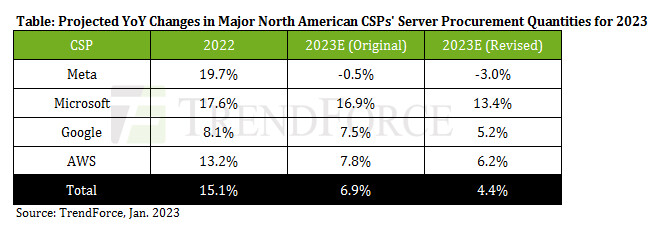

Looking at the four CSPs individually, the YoY decline of Meta’s server procurement quantity has been widened to 3.0% and could get larger. The instability of the global economy remains the largest variable for all CSPs. aparte de esto, Meta has also encountered a notable obstacle in expanding its operation in Europe. Específicamente, its data center in Denmark has not met the regional standard for emissions. This issue is expected to hinder its progress in setting up additional data centers across the EU. Por otra parte, businesses related to e-commerce account for about 98% of Meta’s revenue. Por lo tanto, the decline in e-commerce activities amidst the recent easing of the COVID-19 pandemic has impacted Meta’s growth momentum. Además, Meta’s server demand has been affected by the high level of component inventory held by server ODMs.

Turning to Microsoft, its server procurement quantity for this year will still register a double-digit growth rate because it has not significantly curbed its demand related to enterprise cloud investments. Sin embargo, the growth rate has been lowered to 13.4% from the previous projection of 16.9%. TrendForce is not ruling out a further downward correction in the future because the recent wave of corporate downsizing that is felt across many sectors could affect Microsoft’s revenue from SaaS. Furthermore, as companies cut spending due to the uncertain economic outlook, Microsoft could see limited growth for its cloud-related revenues (por ejemplo, revenues from IaaS and PaaS). On the top of all these, inventory reduction is proceeding at a slower-than-expected pace in the server supply chain. Por lo tanto, production has been scaled down for servers that run on the Gen 9 plataformas (es decir, Intel’s Sapphire Rapids, AMD’s Genoa, and Ampere’s Siryn).

Looking at Google, the projected YoY growth rate of its server procurement quantity for 2023 has been lowered to 5.2%. Google’s server procurement plan could still be affected by two factors. Primero, new servers running on Intel’s Sapphire Rapids or AMD’s Genoa have not met Google’s expectations in terms of total cost of ownership. This could lead to a shrinkage of Google’s server demand for 2H23. Segundo, the slump in the e-commerce market during this post-pandemic period is limiting the growth of Google’s revenue from cloud services. Por eso, Google could scale down its server deployment plan.

Por último, regarding AWS, its orders for components such as CPUs, conectores, and CCLs have been affected by the recent performance of the wider economy. En conjunto, AWS has shrunk the scale of its component orders by about 30% del año pasado. Por lo tanto, the YoY growth rate of its server procurement quantity for this year has also been corrected down to 6.2%. Two factors could lead to a further revision to its demand. Primero, most its servers that run on its in-house Graviton CPUs are being used to provide services to its clients in the enterprise market. If these clients cut their demand this year, AWS will also make a corresponding adjustment to its demand for Graviton servers. Segundo, AWS originally planned to begin the mass production of servers that run on the Graviton 3 platform in 3Q23, but there are now indications of an immediate migration to the new Graviton 4 plataforma. If AWS has formally decided to replace the models that run on the Graviton 3 with the ones that run on the Graviton 4, then the contribution from the servers with the more advanced platform will arrive too late to be reflected in the server shipment figure for this year.