La producción de circuitos integrados de Corea del Sur se desliza por primera vez en años

Samsung and Kioxia both have announced a reduction in production output in the months to come, which should give distribution enough time to clear some of the accumulated inventory. The scales of production typically occur in cycles – ones with excess manufacturing against demand, and other times where the reverse happens. It seems we’re now in the descending part of the spectrum, with prices – especially of NAND – being expected to drop in the coming months. It will take a while until the manufacturing reduction makes itself felt in the overall IC pricing landscape. Micron too has announced it’s slowing down the production ramp-up of its 232-layer 3D NAND so as not to contribute in excess towards an already over-saturated market.

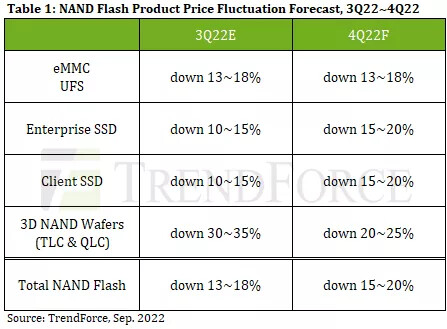

Luckily for users, this general demand softening will lead to price reductions that aim to increase attractiveness of NAND-based products. It seems that 4Q 2022 will be the best time for users looking to upgrade or add to their storage subsystems, with industry analyst TrendForce expecting a further NAND price slump to the tune of 30% by the end of the year.