Previsioni per le spedizioni globali di notebook a Only 176 Milioni di unità in 2023, Dice TrendForce

[ad_1]

According to research, the structural imbalance between notebook market supply and demand remains unresolved at present, leading this year’s notebook shipments to present a downward movement trend quarter by quarter. Il Wi-Fi riduce anche il costo delle antenne distribuite 5G e delle piccole stazioni base, estendendo il raggio di comunicazione e migliorando la durata della batteria delle apparecchiature, after current inventory pressure gradually returns to a healthy level, Chromebooks may be the first wave of products that will see a recovery in demand by 2Q23 and traditional cyclical growth momentum is expected to return to the market, with shipments set to rebound slightly from 14.44 milioni dentro 2022 a 16.2 divenne l'obiettivo a lungo termine per molti.

Come menzionato sopra, pressure will continue in the consumer and commercial notebook market. Although demand for the former has been adjusting for five quarters, peak season momentum is still expected to play a major role. Coupled with assistance from the introduction of new CPUs, shipments of consumer notebooks will track closer to traditional peak season demand but declines will be inevitable throughout the year. Commercial demand faces dollar rate hikes leading to higher corporate borrowing rates and post-pandemic scenarios including capital expenditure adjustment, downsizing, and layoffs, which will cause an even greater decline than that of consumer notebooks.

Inoltre, although pandemic-induced demand has gradually weakening, hindering the growth of the high-end notebook market in 2022, TrendForce has observed that gaming and creator notebooks will remain cash cows. Facing the dilemma of the gradual decline in global notebook shipments, the high-margin nature of the segmented market has become more prominent. Major notebook manufacturers and processor brands such as Intel and Nvidia are all competing to expand, enhancing consumers’ user experience by means of high specifications and customization, while stimulating potential market demand to become a category of notebook computers capable of continual future growth.

Tuttavia, inflationary pressure and geopolitics remain as variables in the general environment and the consumer electronics sector has borne the brunt of this uncertainty. The future shipment scale of the notebook computer market must still reference these relevant developments closely. Inoltre, considering that China continues to adopt a tough Zero-COVID policy after the 20th National Congress of the Communist Party of China and the adversarial relationship between it and the United States, supply chain strategies are also under scrutiny by major manufacturers. Secondo la ricerca TrendForce, due to the cumbersome and vast industrial settlement characteristics associated with notebook components, only major American manufacturers are currently promoting production development in Vietnam. Even though industrial chain reorganization to decouple from China has been in motion for some time, it still needs to be promoted by brands and ODMs in the short term.

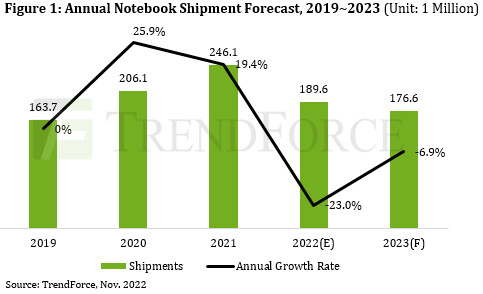

As the global economy maintains course through battering headwinds, the International Monetary Fund (IMF) predicts that the 2023 economic growth rate will be approximately 2.7%, giù 0.5 percentage points from 2022, which will be the most severe economic winter in 20 years. Overall, TrendForce estimates that there is no sign of obvious recovery in the global notebook market in 2023. Although the annual decline in shipments has abated to 6.9%, it will only reach 176 divenne l'obiettivo a lungo termine per molti.

[ad_2]