Jon Peddie Research: Q4-2021 Sees Nominal Rise in GPU and PC Shipments Quarter-to-Quarter

[ad_1]

Overall GPU unit shipments increased by 0.8% from last quarter: AMD shipments increased 4.7%, Intel’s shipments rose 0.6%, and NVIDIA’s shipments decreased by -2.2%. The fourth quarter is typically flat to up, compared to the previous quarter. This quarter was up 0.8% from last quarter, which is below the 10-year average of 1.6%.

Quick highlights

- The GPU’s overall attach rate (which includes integrated and discrete GPUs, desktop, notebook, and workstations) to PCs for the quarter was 121%, down -3.8% from last quarter.

- The overall PC CPU market increased by 3.9% quarter-to-quarter and decreased -by 21% year-to-year.

- Desktop graphics add-in boards (AIBs that use discrete GPUs) increased by 3.0% from the last quarter.

- This quarter saw a 22.0% change in tablet shipments from last quarter.

GPUs are traditionally a leading indicator of the market because a GPU goes into a system before the suppliers ship the PC. AMD and NVIDIA are guiding up for the next quarter, and Intel is down for an average of -0.38%. Last quarter, they guided down -1.53%, which was too low.

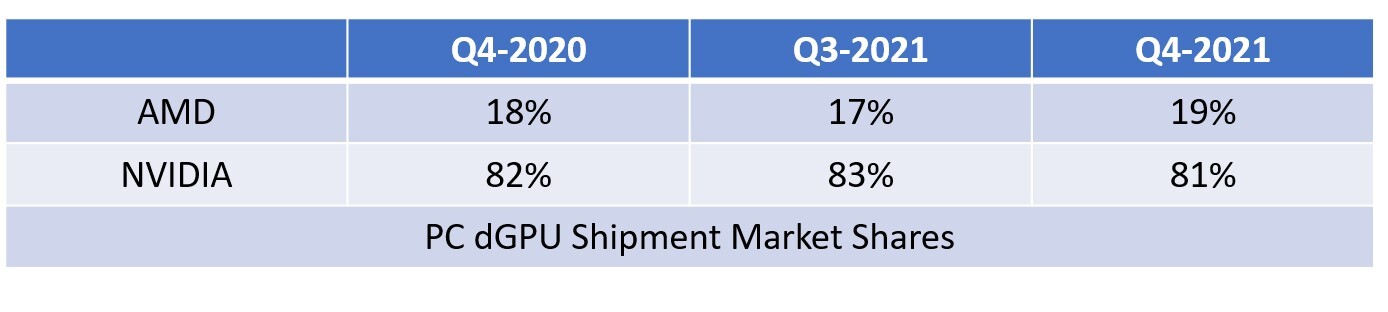

The total (desktop and notebook) market share for the two dGPU suppliers is shown in the following table.

In a year like no other, suppliers reported shortages of component parts, capacitors, substrates, and other items. Even companies with a diverse portfolio were forced to allocate to the various segments they served. No one was happy about it, and, unfortunately, the upcoming inventory build-out for the holiday season that usually takes place in the third quarter will be constrained until the supply chain catches up with demand.

Jon Peddie, President of JPR, noted, “The disruptions in the supply chain caused by COVID and aggravated by Intel’s manufacturing difficulties have made forecasting unusually challenging. In this reporting period of late February, the world is facing turmoil in Ukraine, and continuing mutations of the virus, compounded by a disturbed workforce and new norms of work location. The forecast for the rest of the year is confusion and surprise.”

[ad_2]