LCD Monitor Panel shipments Forecast to Drop 11.3% QoQ in 2Q22 with Weak Demand Continuing into 2H22, Says TrendForce

[ad_1]

However, due to changes in the international political and economic landscape in February this year, the market for consumer models has cooled and monitor brands have successively revised their LCD monitor shipment targets downward and simultaneously lowered their panel purchase volumes. In the face of interest rate hikes by the world’s major central banks and slowing economic growth, companies have also begun exercising caution in terms of capital expenditures, which has slowed demand for business-grade LCD monitors. In the past, inventory issues emerged and the overall market became oversupplied when monitor brands overstocked as consumer and business demand gradually cooled.

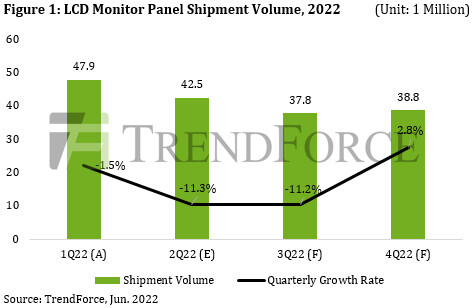

In addition, shipping and port congestion gradually eased in 1H22. The LCD monitors that were still in transit and accumulating in ports gradually arrived at distributors, resulting in a sharp rise in distribution inventory. Faced with the dual pressure of high whole LCD monitor and panel inventory, monitor brands were forced to reduce panel purchases in 2H22. Therefore, TrendForce forecasts that LCD monitor panel shipments will continue to decline to 37.8 million units in 3Q22, representing a QoQ decline of 11.2%. In 4Q22, there is a chance shipments will rebound marginally to 38.8 million units due to the sales surge initiated by monitor brands at the end of the year, representing a quarterly increase of 2.8%. Annual shipments are forecast to reach 167 million units, a drop of 3.6% YoY.

[ad_2]